- HOME

- Accounting Principles

- Balance Sheet – Definition, Example, Formula & Components

Balance Sheet – Definition, Example, Formula & Components

A balance sheet is a financial statement that contains details of a company’s assets or liabilities at a specific point in time. It is one of the three core financial statements (income statement and cash flow statement being the other two) used for evaluating the performance of a business.

A balance sheet serves as reference documents for investors and other stakeholders to get an idea of the financial health of an organization. It enables them to compare current assets and liabilities to determine the business’s liquidity, or calculate the rate at which the company generates returns. Comparing two or more balance sheets from different points in time can also show how a business has grown.

With this information, stakeholders can also understand the company’s prospects. For instance, the balance sheet can be used as proof of creditworthiness when the company is applying for loans. By seeing whether current assets are greater than current liabilities, creditors can see whether the company can fulfill its short-term obligations and how much financial risk it is taking.

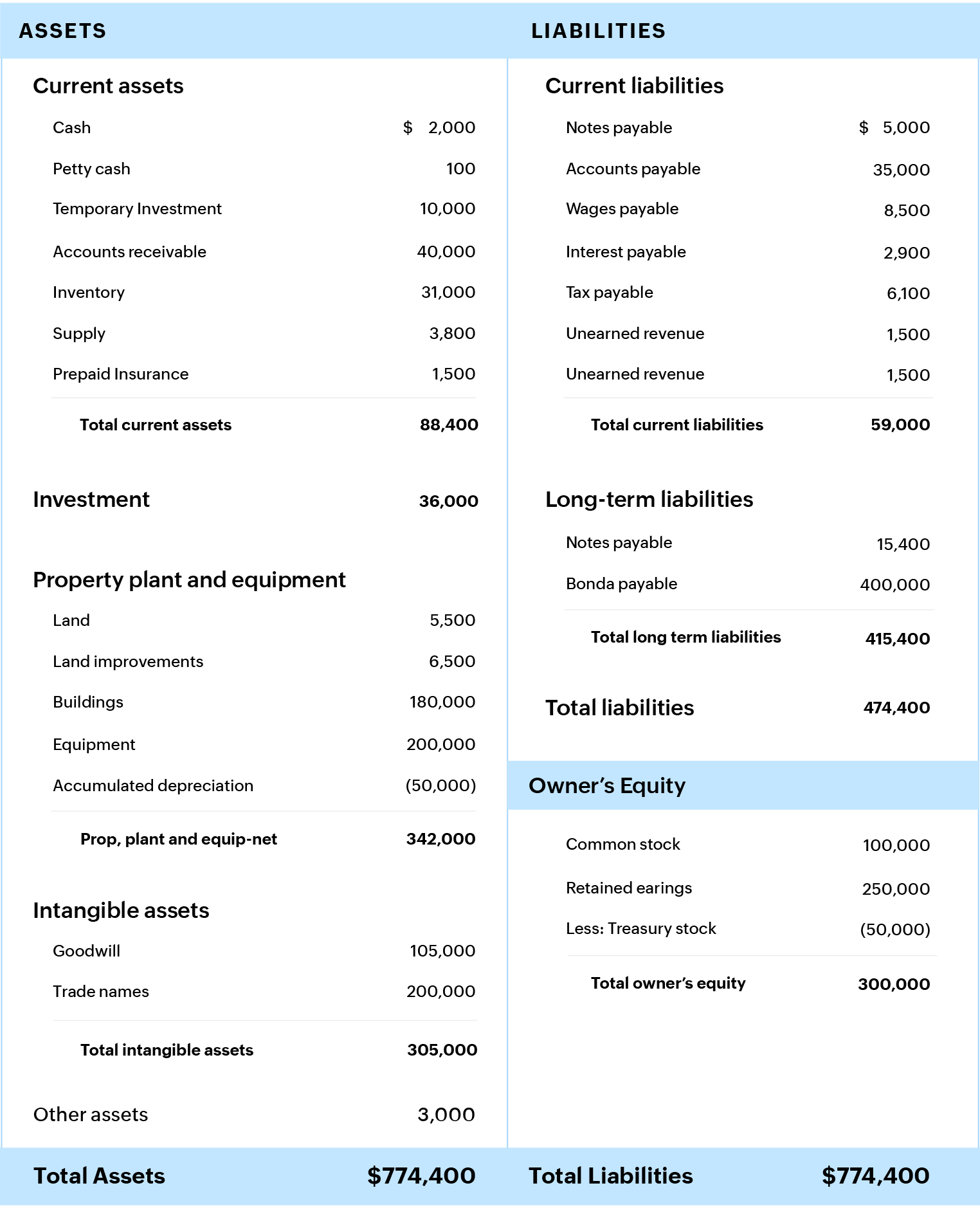

Balance sheet example with sample format

A balance sheet depicts many accounts, categorized under assets and liabilities. Like any other financial statement, a balance sheet will have minor variations in structure depending on the organization. Following is a sample balance sheet, which shows all the basic accounts classified under assets and liabilities so that both sides of the sheet are equal.

Key elements & components of a balance sheet

A balance sheet consists of two main headings: assets and liabilities. Let us take a detailed look at these components.

Assets

An asset is something that the company owns and that is beneficial for the growth of the business. Assets can be classified based on convertibility, physical existence, and usage.

a. Convertibility: This describes whether the asset can be easily converted to cash. Based on convertibility, assets are further classified into current assets and fixed assets.

Current assets: Assets which can be easily converted into cash or cash equivalents within a duration of one year. Examples include short-term deposits, marketable securities, and stock.

Fixed assets: Assets which cannot be easily or readily converted to cash. For example, buildings, machinery, equipment, or trademarks.

b. Physical existence: Assets can be of two types, tangible and intangible.

Tangible assets: Assets which you can see and feel, like office supplies, machinery, equipment, and buildings.

Intangible assets: Assets which do not have physical existence, like patents, brands, and copyrights.

c. Usage: Assets can be classified as operating and non-operating assets.

Operating assets: Assets which are necessary to conduct business operations. For example, buildings, machinery, and equipment.

Non-operating assets: Short-term investments or marketable securities that are not necessary for daily operations.

Liabilities

Liabilities are what the company owes to other parties. This includes debts and other financial obligations that arise as an outcome of business transactions. Companies settle their liabilities by paying them back in cash or providing an equivalent service to the other party. Liabilities are listed on the right side of the balance sheet.

Depending on context, liabilities can be classified as current and non-current.

1. Current liabilities: These include debts or obligations that have to be fulfilled within a year. Current liabilities are also called short-term assets, and they include accounts payable, interest payable, and short-term loans.

2. Non-current liabilities: These are debts or obligations for which the due date is more than a year. Non-current liabilities, also called long-term liabilities, include bonds payable, long-term notes payable, and deferred tax liabilities.

Owner’s Equity/ Earnings

Owner’s equity is equal to total assets minus total liabilities. In other words, it is the amount that can be handed over to shareholders after the debts have been paid and the assets have been liquidated. Equity is one of the most common ways to represent the net value of the company. Part of shareholder’s equity is retained earnings, which is a fixed percentage of the shareholder’s equity that has to be paid as dividends.

The equity value can be positive or negative. If the shareholder’s equity is positive, then the company has enough assets to pay off its liabilities. If it is negative, then liabilities exceed assets.

General sequence of accounts in a balance sheet

According to Generally Accepted Accounting Principles (GAAP), current assets must be listed separately from liabilities. Likewise, current liabilities must be represented separately from long-term liabilities. Current asset accounts include cash, accounts receivable, inventory, and prepaid expenses, while long-term asset accounts include long-term investments, fixed assets, and intangible assets.

Under your current liability accounts, you can have long-term debt, interest payable, salaries, and customer payments, while long-term liabilities include long-term debts, pension fund liability, and bonds payable.

Asset accounts will be noted in descending order of maturity, while liabilities will be arranged in ascending order. Under shareholder’s equity, accounts are arranged in decreasing order of priority.

Balance sheet formula & equation

The balance sheet equation follows the accounting equation, where assets are on one side, liabilities and shareholder’s equity are on the other side, and both sides balance out.

Assets = Liabilities + Shareholder’s Equity

According to the equation, a company pays for what it owns (assets) by borrowing money as a service (liabilities) or taking from the shareholders or investors (equity).

Conclusion

A balance sheet is an important reference document for investors and stakeholders for assessing a company’s financial status. This document gives detailed information about the assets and liabilities for a given time. Using these details one can understand about company’s performance. By analysing balance sheet, company owners can keep their business on a good financial footing.

Now that you have an idea of how values are recorded in several accounts in a balance sheet, you can take a closer look with an example of how to read a balance sheet. In this article, we will discuss different scenarios to understand how values are reflected in the balance sheet accounts.