- HOME

- Taxes & compliance

- The next generation of GST reforms: New GST rates and more!

The next generation of GST reforms: New GST rates and more!

Summary of 56th GST council meeting

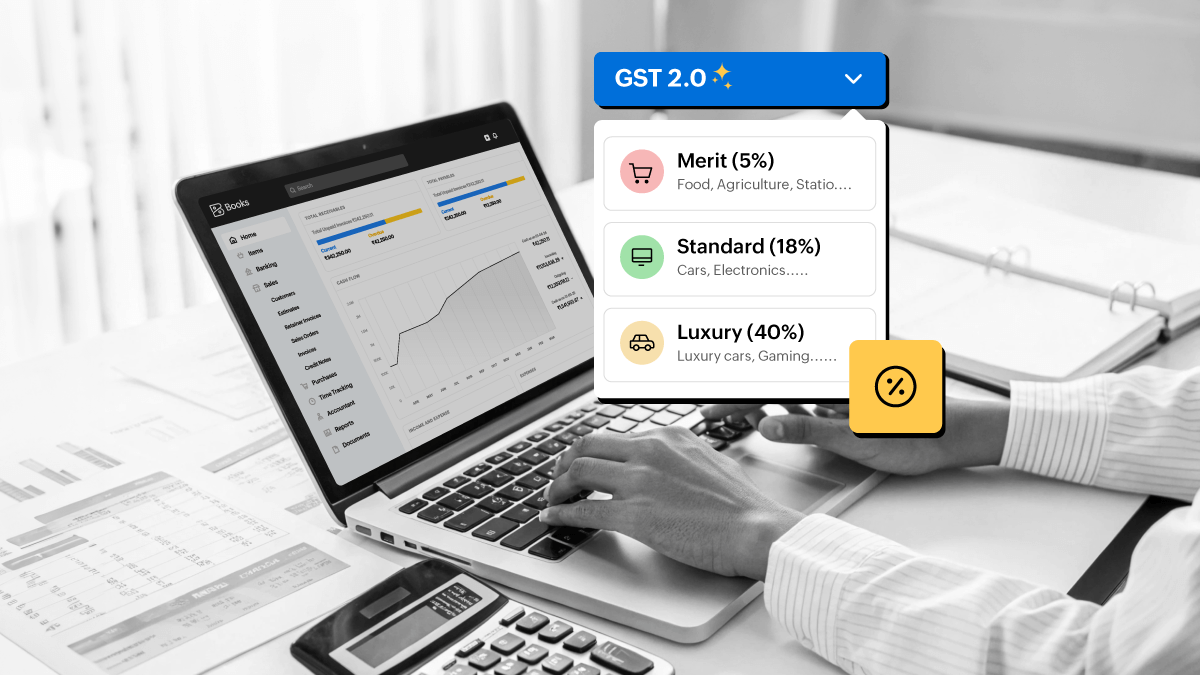

The GST council meeting, which was held on 3rd September 2025, has rationalized the existing GST structure in India. Goods and services now will be taxed based on two tax rates: 5% (merit rate) and 18% (standard rate). In addition to these two tax rates, a 40% GST will be imposed on goods and services that are classified as luxury and sin goods. The existing GST structure follows a four-slab taxation (5%, 12%, 18%, and 28%), which is comparatively complex to the proposed structure. The change in GST rates will be implemented for goods and services supplied on and after September 22, 2025.

The key takeaways from the meeting

The GST rates for most daily essential and agricultural goods have been combined into a 5% tax slab (currently falling under the 12% or 18% slab), with a motive to increase consumption and uplift farmers.

Individual life and health insurance will have nil GST rates, which currently attract an 18% tax rate. This will enhance social benefits for citizens.

Specific medical instruments that currently attract high tax rates of 18% or 12% will now be subjected to a 5% GST rate.

The GST council listed 33 drugs and medicines that will attract nil GST, making them more affordable.

Non-luxury automobiles and important electronic items will be attracting just 18%, down from the current 28% GST.

Basic stationeries related to education, which are currently exposed to high tax rates, will be subjected to nil GST rates.

In addition to the luxury and sin goods, GST rate hikes have been made to goods and services of a few sectors, specifically mining, paper, and textile.

The impact on businesses

The new GST reforms also known as GST 2.0 came as a relief for both households and businesses in India. The reform will lead to increased private consumption, thereby increasing demand for goods and services, especially with the festive season approaching. Businesses can boost their revenue going forward by leveraging this demand. Further, the Department of Consumer Affairs has permitted manufacturers to alter the MRP of unsold goods, ensuring price reductions by capitalizing on the recent GST reform. The reduction in GST rates will improve the tax base and enhance compliance, leading to higher tax revenue. Overall, the reform might be highly beneficial for businesses and households and—in large—our economy.

New GST rates

Food and household sector

Goods/Services | The existing rate | The new rate |

Ultra High Temperature Milk | 5% | NIL |

Pre-packed and labeled chena or paneer | 5% | NIL |

Indian breads | 5% | NIL |

Soap, shampoo, toothbrush, and toothpaste | 18% | 5% |

Tableware and kitchenware | 12% | 5% |

Bicycle | 12% | 5% |

Bhujia, coffee, sauces, pasta, chocolates, preserved meat, butter, ghee, corn flakes, etc. | 12% or 18% | 5% |

Televisions (LED OR LCD above 30 Inches) | 28% | 18% |

Air conditioners | 28% | 18% |

Monitors and projectors | 28% | 18% |

Dishwashers | 28% | 18% |

Agricultural sector

The inverted duty structure has been corrected for fertilizers like ammonia, nitric acid, and sulphuric acid by reducing the GST rate to 5% from 18%.

Goods/Services | The existing rate | The new rate |

Bio pesticides and natural menthol | 12% | 5% |

Tractors | 12% | 5% |

Tractor tyres and parts | 18% | 5% |

Harvesting and threshing machines | 12% | 5% |

Agricultural, horticultural, and forestry machines | 12% | 5% |

Sprinklers and drip irrigation systems | 12% | 5% |

Poultry and bee-keeping machines | 12% | 5% |

Automobile sector

Goods/Services | The existing rate | The new rate |

Two-wheelers <=350cc | 28% | 18% |

Three-wheelers | 28% | 18% |

Small cars: | 28% | 18% |

Buses | 28% | 18% |

Trucks | 28% | 18% |

All automobile parts | 28% | 18% |

Education sector

Goods/Services | The existing rate | The new rate |

Pencils, sharpeners, and crayons | 12% | Nil |

Erasers | 5% | NIL |

Notebooks, exercise books, graph books, maps, and atlases | 12% | NIL |

Geometry boxes, school cartons, and trays | 12% | 5% |

Construction sector

Goods/Services | The existing rate | The new rate |

Cement | 28% | 18% |

Marble blocks | 12% | 5% |

Granite blocks | 12% | 5% |

Sand-lime bricks | 12% | 5% |

Packing cases and wooden pallets | 12% | 5% |

Bamboo flooring/joinery | 12% | 5% |

Travertine blocks | 12% | 5% |

Medical sector

Goods/Services | The existing rate | The new rate |

33 life saving drugs | 12% | NIL |

3 life saving drugs used for cancer and other severe chronic diseases | 5% | NIL |

All other drugs and medicines, including Ayurveda, Unani, and homeopathy | 12% | 5% |

Medical oxygen | 12% | 5% |

Corrective spectacles | 12% | 5% |

Medical, dental, and veterinary devices | 18% | 5% |

Various medical equipment and supply devices like diagnostic kits, bandages, glucometers, reagents, etc. | 12% | 5% |

Insurance sector

Goods/Services | The existing rate | The new rate |

Individual life insurance | 18% | Nil |

Individual health insurance | 18% | NIL |

Service sector

Goods/Services | The existing rate | The new rate |

Hotel accommodation (<= Rs.7500 per unit per day) | 12% | 5% |

Beauty and physical well-being services like yoga centers, salons, gyms, etc. | 18% | 5% |

Textile and handicraft sector

The inverted duty structure has been corrected for manmade fiber and manmade yarn by reducing the GST rate to 5% from 18% and 12% respectively.

Goods/Services | The existing rate | The new rate |

Handy craft statues | 12% | 5% |

Paintings | 12% | 5% |

Sculptures | 12% | 5% |

Wooden, textile, and metal toys | 12% | 5% |

Rate hikes

Here are some of the important products for which the GST rates have been increased.

Goods/Services | The existing rate | The new rate |

High-end cars | 28% | 40% |

Two-wheelers exceeding 350 cc | 28% | 40% |

Aerated, caffeinated, and carbonated drinks | 28% | 40% |

Pan masala | 28% | 40% |

Tobacco products | 28% | 40% |

Online gaming, casino and betting | 28% | 40% |

Click here to learn more about changes in GST rate for more goods/services.

The way ahead

Businesses should try to capitalize on this new generation of GST reform through strategic price reductions to enhance their consumer base. It is crucial for every business to update and take appropriate actions with respect to GST rate changes for the goods and services they are dealing with. The GST Appellate Tribunal will become operational in December 2025, making it vital for businesses to become familiar with its process and procedures for efficient dispute handling. Earlier businesses would be able to claim Input Tax Credit (ITC) if the supplier who sold goods to the business had filed the GST return. But now the ITC claim can be made only if the supplier makes the GST payment for the goods sold. So it is wise for businesses to regularly follow up with suppliers regarding their tax compliance to ensure regular ITC claims. Finally, it is advisable for businesses to leverage the latest accounting tools to streamline their GST process.

FAQs

Are the new GST rates applicable to already manufactured goods?

No, the new GST rates will be applicable for goods supplied on or after 22 September irrespective of the manufacturing date.

Will the new GST rates apply to all goods and services from 22 September?

No, the new rates will be applicable to most goods but not all. A few goods and services, especially those that fall under the sin goods category, will continue with existing GST rates until the central government clears the outstanding loan and interest obligation related to the compensation cess account.

What is Input Tax Credit (ITC)?

Input Tax Credit is the credit obtained by a business for paying taxes on inputs they purchased. They can use this credit to reduce their tax liability.

As an example, consider a business that sells a good with a total tax of Rs.100: To manufacture that good, the business purchased certain inputs for which they paid a tax of Rs. 30. Now, that tax paid for inputs becomes ITC, which can be used to reduce your total tax liability from Rs.100 to Rs. 70.

As per the latest reform, is a business dealing with goods/services that attract a 40% tax rate required to pay the compensation cess?

No, earlier businesses used to pay the compensation cess in addition to GST. Now, the GST rates have been increased to 40%, merging the compensation cess into the newly increased rate. So, businesses will not be required to pay compensation cess separately once the new reform comes into effect.

What is the Inverted Tax Structure?

Inverted Tax Structure occurs when the tax on inputs is higher than the tax on finished goods, creating a disadvantage for businesses as they have to price their products higher to cover the additional tax burden.

Is there any update on the credit notes in the recent GST council meeting?

Yes, the new reform has done away with the requirement of matching credit notes with corresponding invoices, simplifying compliance for the business. However, businesses should ensure the credit notes reflect the GST rate corresponding to the original invoice. For example, if the invoice issued contains the old GST rate, then the credit note should also mention the same rate.

For more clarification, check out the FAQs list released by CBIC via PIB. You can also explore our consolidated article, "FAQs on the new GST rate changes," for deeper insights.