- HOME

- Payment basics

- Real-time payments explained: How they work and why they matter

Real-time payments explained: How they work and why they matter

In July 2025, India’s UPI platform processed a record 19.47 billion transactions worth ₹25.08 lakh crore. That’s over 7,000 payments every second, and a 35 % year-on-year volume jump with a 22 % increase in value. This surge underscores UPI’s growing centrality to India’s digital economy.

For business owners, instant payments via UPI translate to uninterrupted production and agile cash flow—real-time liquidity that transforms operations. This perfect blend of speed, scale, and certainty is what makes real-time payment systems revolutionary.

This quick read breaks down what real-time payments are, why they’re gaining global traction, the challenges they bring, and why businesses should act fast to embrace this space.

Real-time payments explained: How they work and why they matter

What are real-time payments?

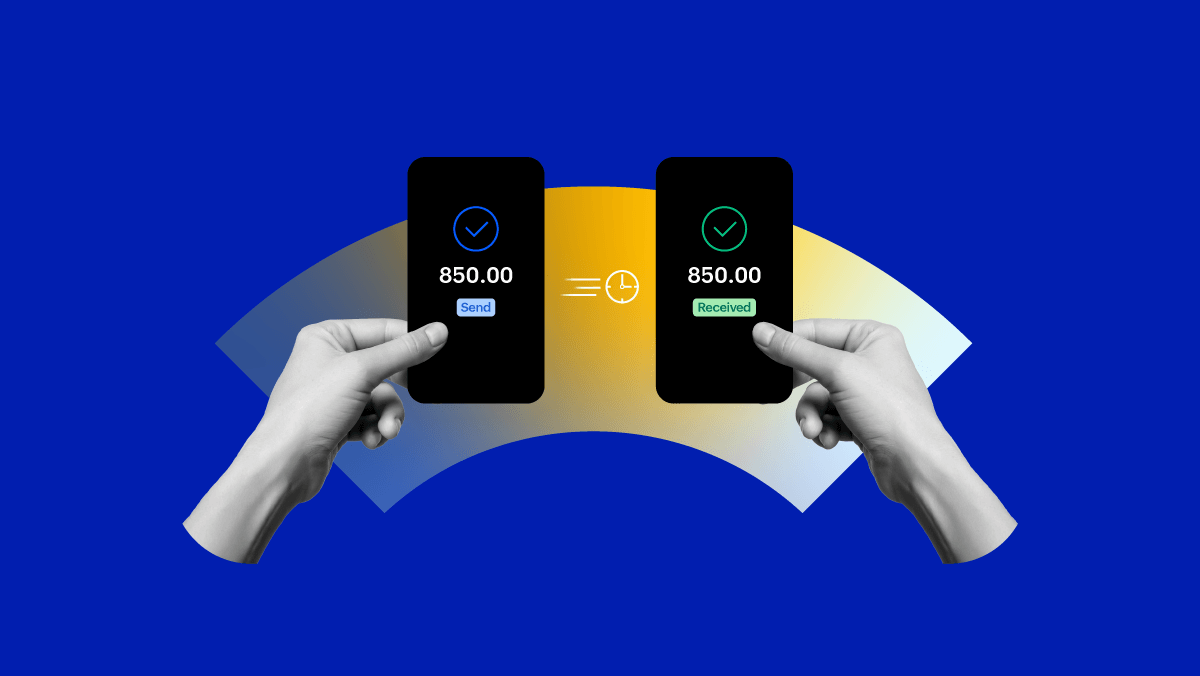

Real-time payments (RTPs) are digital transactions that see authorization, clearing, and settlement completed within seconds at any time of any day. It eliminates the delays tied to business hours or batch processing. In 2023, global RTP volumes surged to 266.2 billion transactions, marking a 42% year-on-year increase, and accounting for nearly one-fifth of all electronic payments worldwide. This share is expected to grow at a phenomenal rate.

How do real-time payments work?

Every RTP transaction typically follows five stages.

Initiation: The payer triggers the transfer via a bank, fintech app, or payment gateway.

Authentication: The payer’s bank verifies the payer's identity and ensures sufficient funds.

Routing: The transaction is routed through an RTP network such as UPI in India, FedNow in the US, or PIX in Brazil.

Settlement: The recipient’s bank credits funds instantly, completing clearing and settlement.

Confirmation: Both the payer and the recipient receive immediate confirmation, with funds available to use straight away.

What makes RTP networks even more valuable is their data-rich messaging capability, powered by ISO 20022 standards. This allows invoices, remittance details, and reference IDs to travel alongside the payment, making reconciliation faster and more accurate for businesses.

Why businesses are adopting RTP

Cash flow certainty: Instant settlement means businesses no longer tie up working capital in pending transactions. Deloitte estimates RTP adoption can improve liquidity forecasts by 20–30%.

Economic impact: ACI Worldwide and Cebr report that RTP delivered $116.9 billion in cost savings and contributed $164 billion to global GDP in 2023 alone.

Operational efficiency: ISO 20022 integration reduces reconciliation effort by up to 80%, according to KPMG, making it easier for corporations to manage payroll, supplier payments, and utilities.

Customer experience: Always-on availability builds trust and loyalty, with surveys showing 70% of SMEs prefer RTP for paying suppliers and vendors.

Real-time payment systems across the world

Real-time payments have taken root globally, but each market has shaped its own story of adoption.

In India, the Unified Payments Interface (UPI) has become more than just a payment system—it’s a platform for innovation. Built on open APIs, it has enabled an entire ecosystem of fintech apps, QR-based commerce, and embedded financial services. For small businesses, UPI has reduced reliance on cash and given them access to digital payments without expensive infrastructure.

The United States has taken a dual-track approach. The Clearing House’s RTP network, launched in 2017, was the first private-sector effort to provide 24/7 instant payments. Building on that, the Federal Reserve introduced FedNow in 2023. Together, these rails are reshaping expectations in a market long dominated by checks and card payments.

In Brazil, PIX has rapidly become the preferred way to pay. Designed and launched by the Central Bank in 2020, it reached mass adoption in record time, and in 2023, it handled 37 billion transactions valued at nearly $4 trillion. Its integration into daily life has reduced reliance on cash and accelerated financial inclusion.

Across Southeast Asia, simplicity has been the key driver. Singapore’s PayNow and Thailand’s PromptPay allow citizens and businesses to transfer money instantly using just phone numbers or national IDs. These systems are now being linked for cross-border payments, making regional commerce faster and more efficient.

In Europe, the SEPA Instant Credit Transfer (SCT Inst) scheme connects 36 countries, enabling euro transfers of up to €100,000 to be completed in under 10 seconds. Adoption continues to climb as banks make instant transfers the default option, creating a unified payments experience across borders.

The United Kingdom, meanwhile, was one of the earliest pioneers. Its Faster Payments system, launched back in 2008, has grown into a trusted national utility, processing millions of transactions every day for both consumers and businesses. It remains a reference point for many newer real-time payment systems around the world.

Together, these examples show a common trajectory. Regardless of geography, real-time payments are evolving from innovation to infrastructure, setting a new global standard for how money moves.

Challenges ahead

While real-time payments promise speed and efficiency, they also introduce new risks and hurdles that businesses and financial institutions must navigate.

Fraud and reversals

A common concern is that instant payments are “irreversible.” In many markets like the US or Europe, that’s largely true. But in India’s UPI system, there are exceptions. If a transaction fails but money is debited, banks are required by RBI guidelines to automatically reverse the amount within one working day. For cases like wrong UPI IDs or fraud, reversals are not automatic. They depend on timely reporting and bank or NPCI intervention under RBI dispute-resolution frameworks. This makes response speed critical for recovery.

Regulatory frameworks

Instant settlement raises new compliance questions around authentication, liability, and dispute handling. Regulators are still evolving policies, and consistency varies across markets.

Digital inclusion

In emerging economies, smartphone access and digital literacy remain barriers. Without inclusive design, RTP risks widening the gap between digitally connected users and those left behind.

These challenges don’t diminish the momentum of RTP but they shape how fast and safely adoption can scale. For providers, the key will be balancing speed with security and innovation with trust.

The way forward

Real-time payments are becoming the backbone of financial infrastructure. Their ability to deliver speed, transparency, and richer data is already reshaping how businesses manage cash and how consumers interact. For businesses, the opportunity is clear. Adopting RTP means better liquidity control, faster supplier payments, and stronger customer trust.

From UPI in India to PIX in Brazil, and FedNow in the U.S., real-time payments are evolving from being a differentiator to becoming a baseline expectation. Businesses that embrace this shift early will not just keep pace but also gain a significant edge in an economy where money moves at the speed of light.