- HOME

- Accounting Principles

- What is a balance sheet and how to read it?

What is a balance sheet and how to read it?

In your company’s annual report, you’ll find a particularly dense section of numbers and tables. This is your balance sheet: a statement released by a company to report its financial health at a given point in time.It is important for accountants and business owners to know how to read and interpret the balance sheet and act on it to avoid negative business outcomes.

Generating a balance sheet

In this section we will take a look at how changes are reflected in the balance sheet under different transaction scenarios.

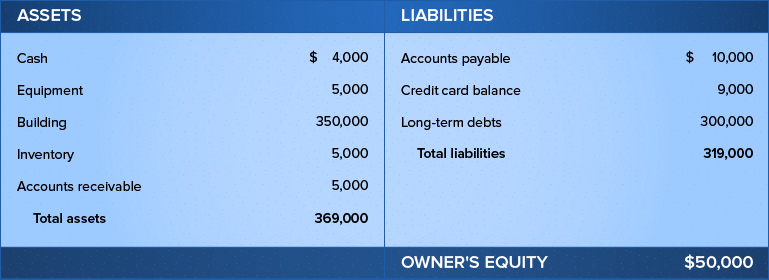

Let us assume that your business is expanding and you need more space to accomodate your employees. For this, you purchase a building for $350,000. After paying $50,000 as a down payment, you apply for a loan from the bank for $300,000. What would the balance sheet look like in this scenario?

The asset column in the balance sheet will show $350,000 irrespective of who owns the asset. By now, you know that a liability is an amount you owe to someone. Since you took a loan from the bank for $300,000, then that amount becomes a liability. It is recorded as a long-term debt on the liabilities side of the balance sheet.

Following is a balance sheet for the day after you purchased the building.

We know that the balance sheet is based on the accounting equation. You can apply the values of assets, liabilities and owner’s equity to check whether assets and liabilities are equal.

Assets ($350,000) = Liabilities ($300,000) + Equity ($50,000)

In this case, the assets and liabilities are equal.

Let us assume another scenario where the property’s value depreciated by $30,000. How will it affect the balance sheet accounts?

The asset account is now reduced by $30,000. The actual value of assets is now $320,000. For the sake of this example, let’s ignore any cash you’ve paid toward your loan and keep the liability value at $300,000. Now we have to adjust the equity value to $20,000.

On applying the values of assets, liabilities, and equity to the accounting equation, you can see that assets are equal to liabilities.

How to read (and analyze) a balance sheet

In the previous section, you noticed how transactions were recorded in the balance sheet in different accounts under assets and liabilities. By now, you also know that the balance sheet functions according to the accounting equation, such that total assets are always equal to the sum of liabilities and owner’s equity.

However, there’s a lot more you can learn from this financial statement, apart from balancing assets and liabilities. Let’s look at some hidden aspects of a balance sheet that determine a company’s finances.

A balance sheet reflects the company’s position by showing what the company owes and what it owns. You can learn this by looking at the different accounts and their values under assets and liabilities. You can also see that the assets and liabilities are further classified into smaller categories of accounts. The value of balance sheet accounts can be used to calculate ratios that show the liquidity, efficiency and financial structure of a business.

Let us take a look at a few of these ratios.

Current ratio: Current assets include cash, petty cash, temporary investments, and inventory, while current liabilities include short term loans, wages payable, and trade creditors. The current ratio is defined as current assets divided by current liabilities. The ideal value for the current ratio is between 1.5 and 2. If the current ratio is too high, then we can infer that the company is hoarding assets instead of using them for expanding the business, which might affect long-term returns. However, businesses must always have sufficient current assets to pay off their current liabilities. If the current ratio goes below 1, then it is difficult for a company to meet its short-term obligations.

Quick ratio: This defines a company’s ability to meet its short-term obligations while making the best out of its liquid assets. It is also called the acid test ratio. The quick ratio is equal to the sum of cash, cash equivalents, short term investments and current receivables divided by current liabilities. A quick ratio equal to 1 is considered normal. This value reflects that the company is equipped with enough assets that can be liquidated to pay off the current liabilities. When the value of the ratio is less than 1, then the company cannot fully pay off its liabilities.

Asset turnover ratio: The asset turnover ratio tells you about the efficiency with which a business utilizes its assets. It determines if a company can generate sales from its assets by comparing net sales with average total assets. A higher asset turnover ratio indicates that the company’s assets are being utilized efficiently to generate sales and make profit for the business. A lower asset turnover means that the company may not be utilizing its assets efficiently, and may experience management or production problems.

Inventory turnover ratio: This ratio indicates the number of times a company sells and replaces its stock during a given period of time. High inventory turnover indicates that the company is selling its products with ease and that those products are still in demand. A low inventory turnover value indicates a decline in demand for the company’s products, and in turn, weaker sales.

Debt-to-equity ratio: This ratio is equal to the company’s total liabilities divided by the owner’s equity. The debt-to-equity ratio helps investors or bankers to decide if they want to lend money to the company. They want to know if the company can generate sufficient cash flow or profit to cover all of its expenses. The debt-to-equity ratio is a clear indicator of a company’s long-term ability to generate sufficient income to fulfill payments and pay off debts. If the ratio is too high, then the company is vulnerable to late interest payments or even bankruptcy.

Conclusion

A balance sheet is an important financial tool that helps investors gain insight into a company and its operations. The transactions are recorded in a balance sheet in such a way that assets are always equal to liabilities. Investors and creditors also refer to the balance sheet and its ratios for getting detailed insights about the business and making informed decisions. A balance sheet is an informative document, but it alone cannot reflect how a company is faring. To get an overall view of a business’ finances, you need to look at the balance sheet along with the income statement and cash flow statement.