- HOME

- Taxes & compliance

- Input Tax Credit (ITC) in Canada: What businesses can claim and how it works

Input Tax Credit (ITC) in Canada: What businesses can claim and how it works

If your business is registered for GST/HST in Canada, Input Tax Credit is one of the main ways you stop sales tax from quietly becoming part of your operating costs.

That sounds simple enough. You pay GST/HST on business purchases, you recover it on the return, and you move on.

In practice, though, this is one of those areas where small mistakes tend to compound. A claim gets made because tax appears on the invoice, not because anyone checked whether the expense is actually eligible. A receipt is kept, but it does not contain the information the CRA expects. A cost is partly personal, partly business, and someone claims the whole amount anyway. Or the claim itself is perfectly valid, but it is made too late or under the wrong accounting method. The tax number may look fine until someone asks what sits behind it. That is usually when things start to wobble.

So the better way to look at ITC is not as a refund button built into GST/HST. They are a claim, and like most claims, they depend on conditions, records, and timing. When those pieces are in place, ITC works as it should. When they are not in place, the business can end up recovering less than it should, or claiming more than it can support.

What ITC actually does

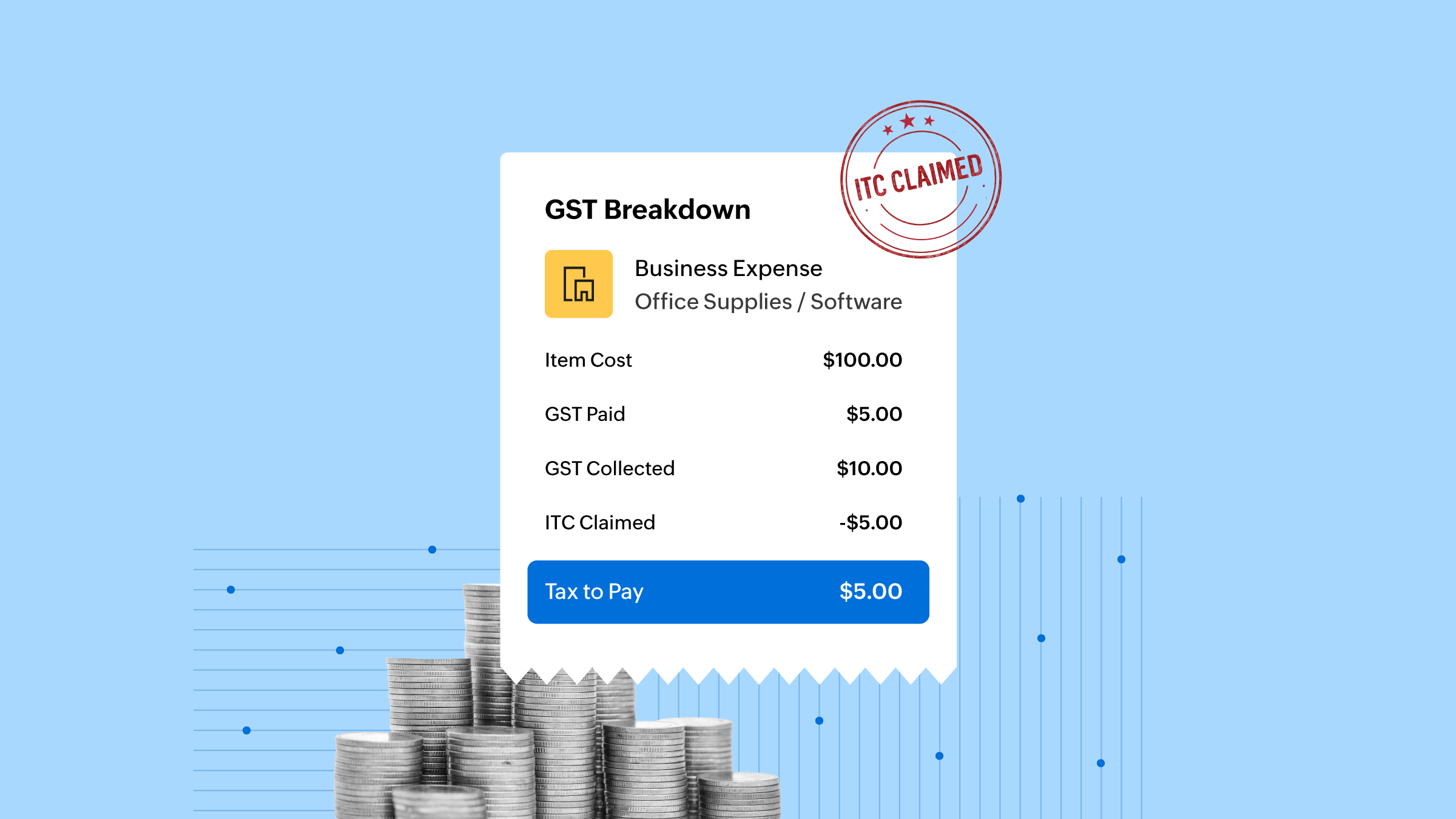

At a practical level, ITC reduces the GST/HST your business has to remit.

Your business collects GST/HST on taxable sales. At the same time, it may be paying GST/HST on purchases and expenses used in its commercial activities. ITC is how you recover the eligible tax paid on those costs. The result is that your return reflects the tax you collected, net of the tax you were entitled to recover. That is why ITC affects cash flow so directly. They are not just a technical feature of the return. They change how much tax leaves the business.

It also helps to be clear about what ITC is not. It is not a blanket right to recover every bit of GST/HST that passes through the business. The CRA’s own guidance frames eligibility around specific conditions: the registrant has to be entitled to claim ITC, the purchase has to relate to commercial activities, the right records have to exist, and the claim has to be made within the time limit.

The first thing to check: Can the business claim ITC at all?

The answer starts with registration.

In general, a business has to be a GST/HST registrant to claim ITC. The CRA also provides rules for new registrants. If a business was a small supplier before registration, it may be able to claim ITC on certain property it had on hand when registration began, including some inventory, real property, and capital property. But that does not extend to everything. Services supplied before registration and rent relating to a period before registration are not treated the same way.

That is worth pointing out because businesses sometimes assume registration simply opens the door to all recent pre-registration costs. It does not. The CRA’s rules are more selective.

There is also another filter that matters just as much: the purchase has to relate to the business’s commercial activities. If something is used fully in commercial activities, the claim is usually stronger. If it is partly personal, partly exempt, or partly non-commercial, the claim may need to be reduced. The CRA says you can generally claim ITC only to the extent that the property or service relates to use, consumption, or supply in commercial activities.

That “to the extent” language matters. It is the difference between a full claim and a partial one.

What businesses commonly claim

This is where the topic starts to feel familiar again.

In normal business life, ITC is often claimed on ordinary operating costs: rent, office expenses, software, equipment, advertising, utilities, professional fees, and inventory purchases used in taxable commercial activities. Broadly speaking, if the business is registered and the cost is genuinely connected to commercial activity, the GST/HST on that purchase may be recoverable.

That broad rule is useful, but it is also where people get too comfortable. The existence of a business purpose does not mean every claim works the same way. Some categories are restricted. Some need apportionment. Some require more careful support than businesses expect.

That is why ITC questions are often less about whether the purchase was “for the business” in a general sense and more about the exact nature of the expense.

Meals and entertainment: Business-related does not mean fully claimable

This is one of the clearest examples of exemptions.

Many owners assume that if they take a client to lunch or incur entertainment costs in a business setting, the GST/HST is recoverable in full. In many cases, that is not how the CRA treats it. The CRA’s ITC calculation guidance says that for meals and entertainment expenses, you can claim 50% of the actual GST/HST paid during the reporting period under the standard method described there, though exceptions do exist.

So a dinner meeting may still support an ITC, but usually not for the full tax amount. That is the kind of detail that gets missed when the books are handled too quickly.

This is exactly why ITC cannot be treated as an automatic claim. A purchase may be ordinary and entirely business-related, but still only partly recoverable.

Motor vehicles: Another common trouble spot

Vehicle claims are one of the places where ITC often becomes more complicated than businesses expect.

The CRA’s guidance on eligibility percentage and motor vehicles points to business-use questions and other restrictions. For example, where a passenger vehicle is used 10% or less in commercial activities, a registrant other than a financial institution is generally not entitled to claim ITC for that vehicle. The rules around specified motor vehicles and related costs can also make this area more restrictive than owners first assume.

Another common misunderstanding occurs when a business leases or buys a passenger vehicle, the vehicle is used in the business in some way, and the GST/HST is claimed in full. But if the business use is mixed, or the vehicle falls into one of the categories where restrictions apply, the answer is not automatically “yes.”

This is one of those areas where a claim can feel reasonable and still be wrong in detail.

The documents matter more than the payment

This is one of the quietest ways otherwise valid claims weaken.

Businesses often have no trouble proving that a purchase was made. The bank statement exists. The card statement exists. The transfer went through. What they do not always have is the documentary support the CRA expects for ITC.

The CRA’s documentary requirements are explicit. Depending on the amount of the purchase, the records generally need to show details such as the supplier’s name, invoice date, amount paid or payable, the amount of GST/HST, a description of what was supplied, and in many cases the supplier’s GST/HST registration number. CRA publications also note recent changes and continued emphasis on having the required information on invoices, receipts, contracts, or other supporting documents.

That is why proof of payment is not enough on its own. It proves that cash left the business. It does not necessarily prove that ITC is properly supported.

In practice, many ITC problems are not really about tax interpretation. They are about incomplete records.

Timing is part of the claim too

Even a valid ITC claim can become awkward if it sits unresolved too long.

The CRA’s ITC guidance includes time limits for claiming ITCs. The exact window can vary depending on the nature of the registrant, and larger businesses and certain financial institutions can face shorter claim limits than others. The broad practical point is that businesses should not leave claims unreviewed for long periods just because they know tax was paid.

This matters because late claims tend to come with weaker records. The invoice is harder to locate. The purpose of the purchase is less obvious. The staff member who handled it may not remember the context. What looked like a simple recoverable amount turns into a reconstruction exercise.

That is one reason periodic review helps. Businesses that leave ITC to the end of the year often create more work for themselves than businesses that review them monthly or quarterly.

The quick method changes the ITC answer

This is another place where assumptions can go wrong.

If the business uses the quick method of accounting, the normal pattern of claiming ITC changes. The CRA says businesses using the quick method cannot claim ITC on operating expenses in the usual way. They may still be able to claim ITC on certain purchases, including some capital items, land, and some purchases eligible for capital cost allowance, but the operating-expense logic is different.

That means “Can we claim the GST/HST on this?” is not a complete question until you know which reporting method the business is actually using.

The answer under the regular method and the answer under the quick method may not be the same.

A few practical examples

It helps to slow this down and look at ordinary situations.

A business buys new laptops for their staff. The business is registered, the laptops are used fully in commercial activities, the supplier invoice is complete, and the claim is made in time. That is the kind of fact pattern where ITC usually makes sense.

Now, take a restaurant bill from a client meeting. The expense may still be legitimate, but the GST/HST treatment is likely more limited because meals and entertainment claims are generally restricted to 50% under CRA rules.

Take a passenger vehicle used partly for business and partly for personal use. That is where many businesses want a simple answer and do not get one. The GST/HST paid may not be fully claimable, and in some cases the claim may be blocked or reduced because of the underlying vehicle rules and business-use threshold.

Software renewals, paid annually, in advance is another example. The payment is obvious. The tax is obvious. The harder question is whether the records and reporting process are clear enough that the ITC claim can still be understood later.

That is often what this comes down to.

Where ITC sits on the return

ITC is not a side note. It directly affect the GST/HST return.

CRA instructions for preparing the return explain that ITC usually goes through line 106, adjustments through line 107, and the combined figure is reported on line 108. That total then affects the net tax position of the businesses. This is worth noting businesses sometimes think of ITC as something that sits quietly in the expense records. It does not. A wrong ITC changes the return itself.

Why this often turns into a workflow issue, not a tax issue

By the time an ITC problem becomes obvious, the underlying mistake is often not “we misunderstood tax law.” It is usually something smaller:

The invoice was not saved properly.

The tax code was used inconsistently.

The expense was partly personal and no one documented the split.

The business left the review too late.

A valid purchase was made, but the support behind it was weak.

That is why this topic so often comes back to process. The more consistent the expense capture, coding, document attachment, and review cycle, the easier it is to properly handle ITC.

Where software actually helps

Software does not make the tax judgment for you. It does not decide whether a claim is valid. It does not replace the need to understand the CRA’s rules.

What it can do is reduce the amount of disorder around the claim. If purchase records are clean, tax amounts are visible, vendor details are organized, supporting documents are attached to transactions, and the return can be reviewed without digging across multiple systems, a lot of the everyday friction behind ITC mistakes starts to disappear.

That is where a tool like Zoho Books can be genuinely useful. Not because it magically solves ITC, but because it gives businesses a more structured place to capture expenses, attach invoices and receipts, review tax coding, and keep the accounting side of the claim from becoming fragmented.

That kind of structure is often what businesses are missing.

In summary

ITC is one of the main ways a GST/HST-registered business avoids carrying sales tax as a permanent cost.

But the fact that tax was paid is only the starting point.

A proper claim depends on registration, business use, any applicable restrictions, the right documents, the right timing, and the right reporting method. When those pieces are in place, ITC works the way businesses expect it to. When they are not, even ordinary expenses can become messy to defend.

The tax amount is not the whole story. The support behind the claim matters just as much.