- HOME

- Banking & payments

- What is Bank Reconciliation and what should you know about it?

What is Bank Reconciliation and what should you know about it?

What is bank reconciliation?

Bank reconciliation is the process by which a business compares its financial accounts with its bank statement to ensure all money going in and out of the business is reflected accurately in both places. In most cases, a bank reconciliation statement is generated to compare these records and make adjustments if necessary.

Why bank reconciliation is essential for SMBs

Reconciling bank accounts can admittedly be monotonous, but it needs to be done on a regular basis. When you reconcile your books with your bank statement, it acts as a kind of reality check for your business. You can:

- Verify that your payables and receivables have been entered correctly and identify if there are any duplicate entries or irregularities

- Determine if any of your checks were duplicated, sent without the correct authorization, or never deposited, giving you the jump on any fraudulent activities that may be happening

- Calculate an accurate total of the cash in your account, helping you to avoid unnecessary fines from the bank claiming insufficient funds

- Observe when you receive payments and when the deposited amount actually gets reflected in your bank account, allowing you to devise better plans for payment collection from late customers

- Obtain confirmation that your financial statements are precise so you can file accurate tax returns on time

How often should you reconcile your bank accounts?

In general, it’s good practice to perform bank reconciliations at the end of each month. This is a convenient time because banks generally send monthly statements at the end of each month, which can be compared with your books. Companies with higher fraud risks can choose to do weekly or daily reconciliations to ensure that cash is moving in and out of the business in the right way. If you have a seasonal business, on the other hand, then you can even opt to do the reconciliations during the less busy months of the year.

The reconciliation process

Before you sit down to reconcile your books, make sure your bank records and book of accounts are updated. Here are a few quick steps on how you can reconcile your accounts and create a bank reconciliation statement.

Step 1: Check the cash balances on both documents

First compare the transactions in your books to the bank statement. The ending balance in both these documents should be the same for a given period of time, be it a month or week.

For example, if the bank statement issued for the month of August 2021 states that the final balance is $9,000, then your closing balance in your books should also reflect $9,000.

Step 2: If they don’t match, identify transactions that are causing the differences

There is always a chance that some transactions that have been listed by the bank are not yet recorded in your books and vice versa. It’s common to find mismatches when:

- The checks received and recorded by your business have yet to be updated on the bank statement

- There is a difference between the date that a check gets deposited by the creditor and the amount gets credited into the bank account

- The service charge deducted by the banks on your transactions have yet to be accounted in your books

- There is a mistake in the debited or credited amount recorded by the bank

For example, let us assume that your account reflects $9,100 while your bank statement reflects $9,000. When you check your transactions, you realize that the excess $100 is because the bank has charged a total transaction fee which you haven’t added to your account statement.

Step 3: The reconciliation

This is where you make adjustments to fix discrepancies like the example gave above. You must ensure that the money coming in or going out of your business is listed in both your bank statement and accounting records. If there are transactions in the bank statement that are not in your books, you must add them.

Simultaneously, make note of transactions that are present in your books but not in your bank statement. A few such instances include deposits in transit and outstanding checks. Such banking errors should be modified so that the right amount gets reflected.

The next step is to make adjustments to the ledger. For every change that you identified on the bank statement, check if you have relevant receipts of those payment line items. There are times when the bank may have charged you for something, like bank fees or service charge, and you may not have added them to the ledger.

When adjustments are made and the cash balance in your books matches the bank statement, this is an indication of good financial health.

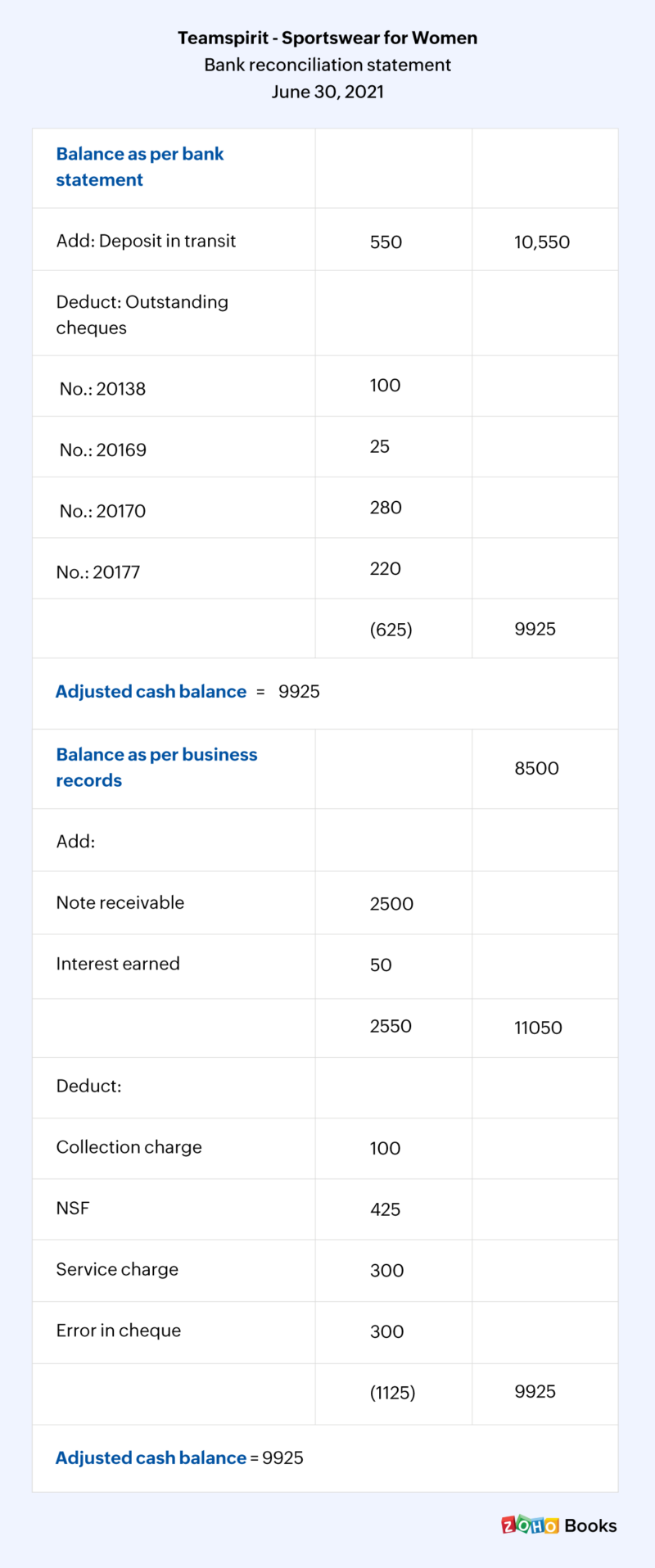

Bank reconciliation example

Let us assume that Teamspirit Pvt Ltd, a sportswear business, is closing its books on June 30, 2021. The bank statement shows the cash balance as $10,000 and the ledger shows $8,500. The reason for $1,500 discrepancy is as follows:

- An $550 deposit was sent to the bank on June 30, 2021, which does not appear in the statement because it is still in transit.

A few checks that were not cleared by the bank for June are:

- A note receivable amount of $2,500 was collected by the bank on behalf of the business.

- The bank has earned another $50 as interest on the average account balance for June.

- The bank has been charged $100 for collecting the note.

- The $425 check deposited by the business has been charged back by the bank as NSF (non-sufficient funds).

- The bank has also deducted $300 as a service charge.

- A check issued to fix your store’s interior has an error. The issued check has an amount $500 while the entry in the journal is recorded as $200.

Using the above inputs, we need to prepare a bank reconciliation statement, adjusting the journal entries according to the bank statement.

Challenges with manual reconciliation

There are several reasons why manual reconciliation should be avoided. Some of them are:

- Reconciliation, when done manually, is error-prone. There are several mistakes that are possible, like wrong entries being made into the existing accounts. You either end up spending too much time fixing these errors or end up with inaccurate financial records.

- Some businesses with short reconciliation cycles tend to share incomplete data for analysis. Accountants, who analyze this fragmented information, add in their own inputs based on their assumptions. The inconsistencies due to guesswork cause errors. The complexity of the situation increases further when the size and volume of your business increases.

- Your business may face several situations where you are not directly responsible for discrepancies between company records and financial records. Some of these situations include incorrect product delivery, projects not reaching milestones on time, and more. If there is no real time visibility into this information, then the finance team will not catch the reason/context behind the inconsistency in data.

Takeaway

The main goal of reconciling your bank accounts is to identify variances between the amount of cash in your bank and the amount you have in your business account. Reconciliation will help you identify if any checks have bounced or were cashed without your knowledge, pick out fraudulent transactions, and report both situations on time. Doing this religiously will keep your books error-free before the annual audit cycles, where auditors examine your records as a part of their routine analysis.