- HOME

- Inventory Management

- What is Manufacturing Overhead Cost?

What is Manufacturing Overhead Cost?

Manufacturing overhead (MOH) cost is the sum of all the indirect costs which are incurred while manufacturing a product. It is added to the cost of the final product along with the direct material and direct labor costs. Usually manufacturing overhead costs include depreciation of equipment, salary and wages paid to factory personnel and electricity used to operate the equipment.

According to GAAP (generally accepted accounting principles), manufacturing overhead should be included in the cost of finished goods in inventory and work in progress inventory on a manufacturer’s balance sheet and in the cost of goods income statement.

What are the different types of indirect costs related to manufacturing overhead?

Manufacturing overhead costs are called indirect costs because it’s hard to trace them to each product. These costs are applied to the final product based on a pre-determined overhead absorption rate. Overhead absorption rate is the manufacturing overhead costs per unit of the activity (also called as the cost driver) like labor costs, labor hours and machine hours. Here are the types of costs that are included in manufacturing overhead:

Indirect labor

Indirect materials

Utilities

Physical costs

Financial costs

Indirect labor

Indirect labor is the cost to the company for employees who aren’t directly involved in the production of the product. For example, the salaries for security guards, janitors, machine repairmen, plant managers, supervisors, and quality inspectors are all indirect labor costs. Cost accountants derive the indirect labor cost through activity-based costing, which involves identifying and assigning costs to overhead activities and then assigning those costs to the product.

For example, in activity based costing, every employee who is working in the manufacturing facility but not directly involved in the manufacturing process, keeps a log on the amount of hours spent on their job and from that the total cost is calculated and then the cost is assigned to each product being manufactured.

Indirect materials

This cost is incurred for materials which are used in manufacturing but cannot be assigned to any single product. Indirect material costs are mostly related to consumables like machine lubricants, light bulbs , and janitorial supplies. Cost accountants spread these costs over the entire inventory, since it is not possible to track the individual indirect material used.

For example, in a paper factory, the wood pulp used isn’t counted as an indirect material as it is primarily used to manufacture paper. But the lubricant used to keep the machinery running properly is an indirect cost incurred during the manufacture of paper.

Utilities

Utilities such as natural gas, electricity, and water are overhead costs that fluctuate with the quantity of materials being produced. The might increase or decrease depending on the demand for the product in the market. Since their usage isn’t constant, they’re included as variable overhead costs. Accountants calculate this cost for the whole facility, and allocate it over the entire product inventory.

Physical costs

These costs include the physical items which are essential for manufacturing. They usually include the cost of the property where the manufacturing is taking place and its depreciation, purchasing new machines, repair costs of new machines and other similar costs. Accountants calculate this cost by either the declining balance method or the straight line method. In the declining balance method, a constant rate of depreciation is applied to the asset’s book value every year. The straight line depreciation method is used to distribute the carrying amount of a fixed asset evenly across its useful life. This method is used when there is no particular pattern to the asset’s loss of value.

Financial costs

Financial overhead consists of purely financial costs that cannot be avoided or canceled. They include the property taxes government may charge on your manufacturing unit, audit and legal fees, and insurance policies. These costs don’t frequently change, and they are allocated across the entire product inventory.

Fixed, variable and semi-variable overheads

Manufacturing overhead is classified into different parts based on its behavior. Some overhead costs change with the amount of output produced, while others don’t. This creates three types of overhead cost based on behavior:

Fixed overhead costs: These costs don’t fluctuate based on the manufacturing output.

Variable overhead costs: These costs are dependent on the output.

Semi-variable overhead costs: These costs are partially variable and partially fixed.

Fixed overhead costs

These overhead costs don’t fluctuate based on increases or decreases in production activity or the volume of output generated during manufacturing. These overhead costs aren’t influenced by managerial decisions and are fixed within a specified limit based on previous empirical data. They include equipment depreciation costs during manufacturing, rent of the facility, land used for inventory, and depreciation of the facility.

Variable overhead costs

These overhead costs vary in proportion to the volume of output generated. They’re directly affected by the volume of the output produced or stored. They include shipping expenses, advertising and marketing costs for the product, and electricity used during manufacturing.,

Semi-variable overhead costs

Semi-variable overhead costs are partially variable and partially fixed in nature. Since they contain both a fixed and variable component, it doesn’t change directly in proportion to the manufacturing output. For example, telephone charges, repairs and maintenance of the equipment etc.,

How to calculate manufacturing overhead cost

You can calculate manufacturing overhead cost either as a total for the entire production facility, or on a per-unit basis:

Determining total manufacturing overhead cost

To determine your total manufacturing overhead cost, you need to add up all of the overhead costs for your manufacturing facility. Let’s look at an example:

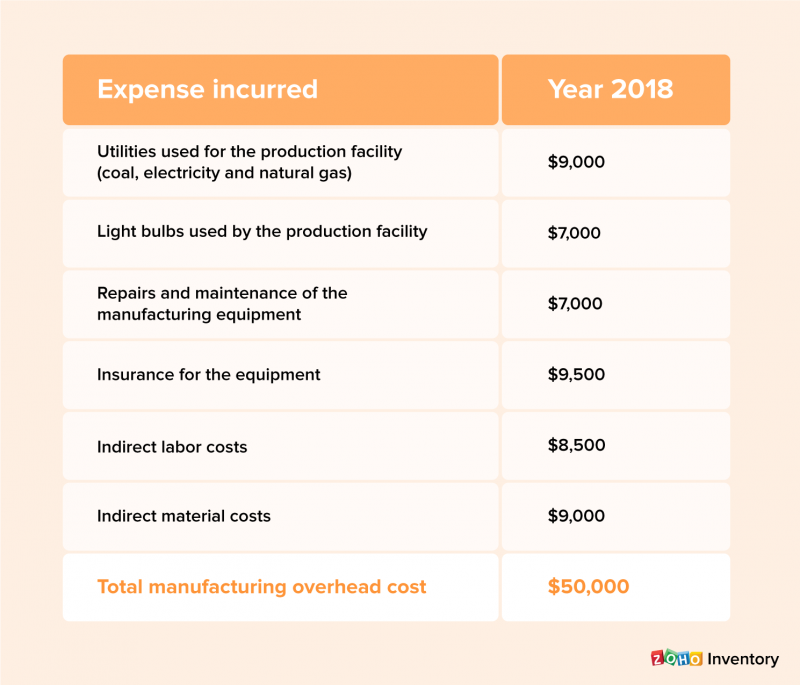

A company made 10,000 bicycles in 2018. Here is the breakdown of overhead expenses incurred at their manufacturing facility in 2018:

To calculate the total manufacturing overhead cost, we need to sum up all the indirect costs involved. So the total manufacturing overhead expenses incurred by the company to produce 10,000 units of cycles is $50,000.

To find the manufacturing overhead per unit

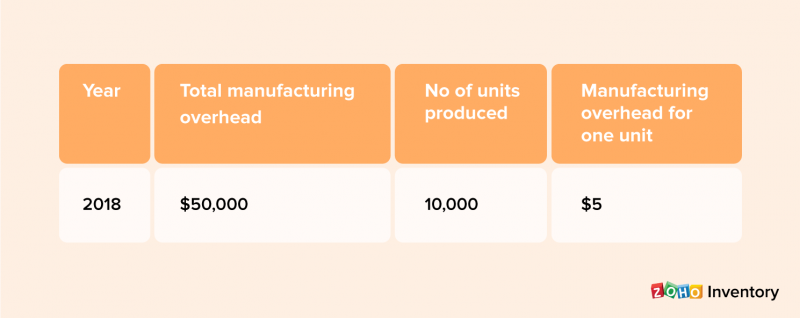

In order to know the manufacturing overhead cost to make one unit, divide the total manufacturing overhead by the number of units produced.

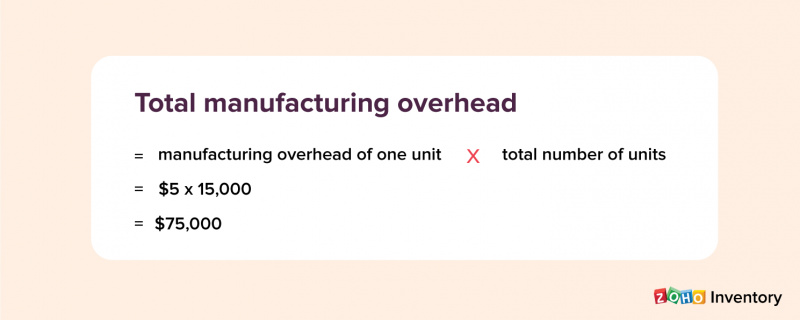

The total manufacturing overhead of $50,000 divided by 10,000 units produced is $5. So, for every unit the company makes, it’ll spend $5 on manufacturing overhead expenses on that unit.

If it plans to produce 15,000 units the next year, the total manufacturing overhead can be predicted by multiplying the manufacturing overhead of one unit by the total number of units it intends to produce.