GSTR-3B : Temporary monthly GST return containing the consolidated details of all inward and outward supplies

- What is the GSTR-3B?

- Dates associated with the GSTR-3B.

- Prerequisites of the GSTR-3B.

- Contents of the GSTR-3B.

What is GSTR-3B?

The GSTR-3B is a consolidated summary return of inward and outward supplies that the Government of India has introduced as a way to relax the requirements for businesses that have recently transitioned to GST. Since a lot of small and medium businesses have been using manual accounting methods, filing returns within the July 2017 deadlines would be difficult for many of these businesses. Hence, in the months of July and August 2017, the tax payments will be based on a simple return called the GSTR-3B.

Dates associated with the GSTR-3B

The GSTR-3B should be filed twice, by the 20th of August and the 20th of September. GSTR-3B for July should be filed by the 20th of August, and the GSTR-3B for the month of August should be filed by the 20th of September. Remember that the introduction of the GSTR-3B does not eliminate the need to file the GSTR-1 and GSTR-2 during these two months. The dates for filing the GSTR-1 and GSTR-2 for the months of July and August 2017 have been scheduled as follows:

Dates for filing returns for the month of July:

GSTR-3B: 20th August

GSTR-1: 5th September

GSTR-2: 10th September

GSTR-3: 15th September

Dates for filing returns for the month of August:

GSTR-3B: 20th September

GSTR-1: 20th September

GSTR-2: 25th September

GSTR-3: 30th September

Prerequisites of the GSTR_3B

The GSTR-3B form should be submitted by any business that is liable to file the monthly returns GSTR1, GSTR-2 and GSTR-3. The GSTR-3B form can be easily filed online through the GSTN portal. The tax payable can be paid through challans in banks or online payment.

Contents of the GSTR-3B

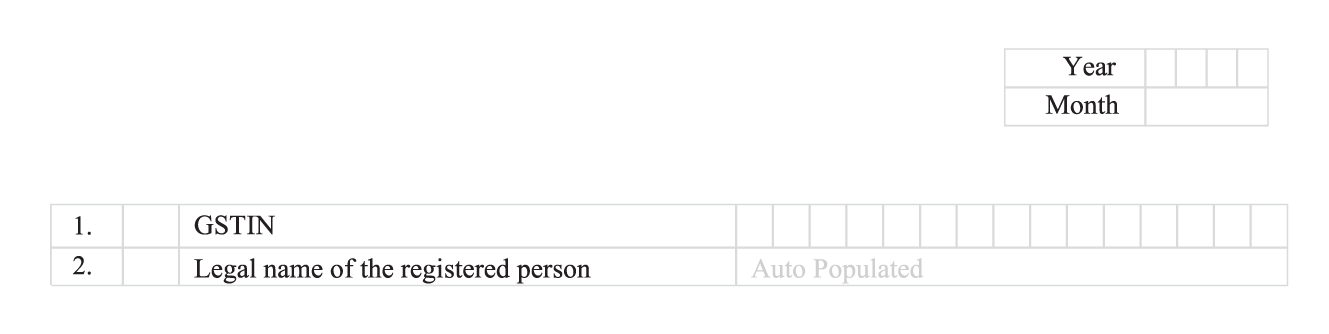

On the GSTR-3B, you will have to provide your GSTIN and legal name, and complete other tax-related sub-sections such as:

1. Details of your sales and purchases which are liable for reverse charge

On the GSTR-3B, you will have to provide your GSTIN and legal name, and complete other tax-related sub-sections such as:

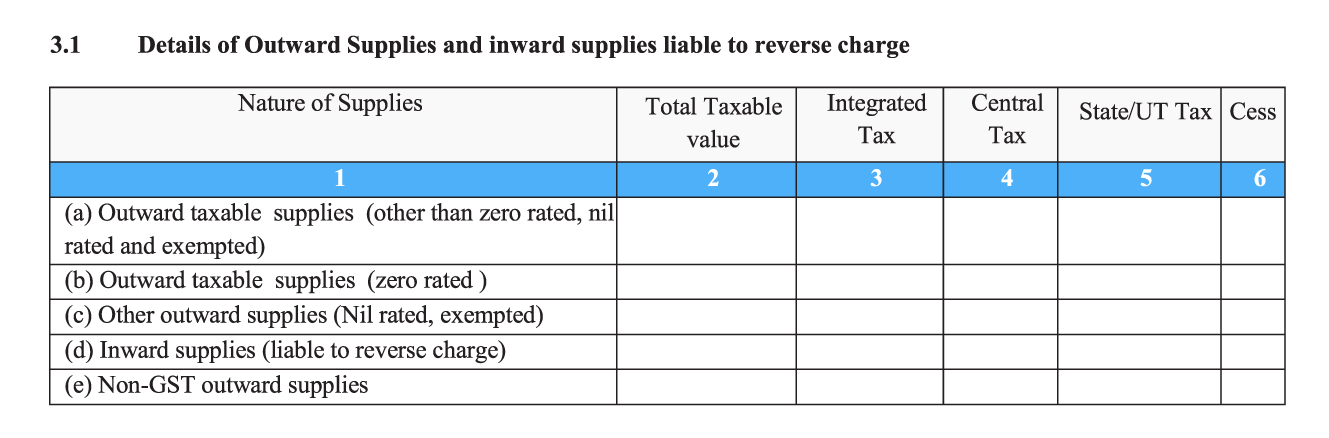

1. Details of your sales and purchases which are liable for reverse charge

In this section, you will have to enter the total taxable value (equal to the value of invoices + debit notes - credit notes + advance tax received), IGST, CGST, SGST, and cess for the following:

* Sales supplies (zero rated)

* Sales supplies (other than zero rated, nil rated and exempted)

* Other sales supplies (nil rated and exempted)

* Purchase supplies liable for reverse charge

* Non-GST sales supplies (for example, petrol)

Cess is applicable to certain industries such as automobiles and tobacco. If your business is not involved in selling such goods, there’s no need to enter cess-related details.

Zero-rated supply includes export of goods and/or services or supply of goods and/or services to an SEZ developer or SEZ unit. It’s important to remember that nil-rated and exempted goods and/or services under GST are not the same. Nil-rated products are not taxed at the time of sale, but input tax credit can still be claimed for them. Exempted products are not taxed at the time of sale, and no input tax credit can be claimed for them.

2. Details of inter-state sales made to unregistered buyers, buyers registered under the composition scheme, and UIN (Unique Identification Number) holders.

In this section, you will have to enter the total taxable value (equal to the value of invoices + debit notes - credit notes + advance tax received), IGST, CGST, SGST, and cess for the following:

* Sales supplies (zero rated)

* Sales supplies (other than zero rated, nil rated and exempted)

* Other sales supplies (nil rated and exempted)

* Purchase supplies liable for reverse charge

* Non-GST sales supplies (for example, petrol)

Cess is applicable to certain industries such as automobiles and tobacco. If your business is not involved in selling such goods, there’s no need to enter cess-related details.

Zero-rated supply includes export of goods and/or services or supply of goods and/or services to an SEZ developer or SEZ unit. It’s important to remember that nil-rated and exempted goods and/or services under GST are not the same. Nil-rated products are not taxed at the time of sale, but input tax credit can still be claimed for them. Exempted products are not taxed at the time of sale, and no input tax credit can be claimed for them.

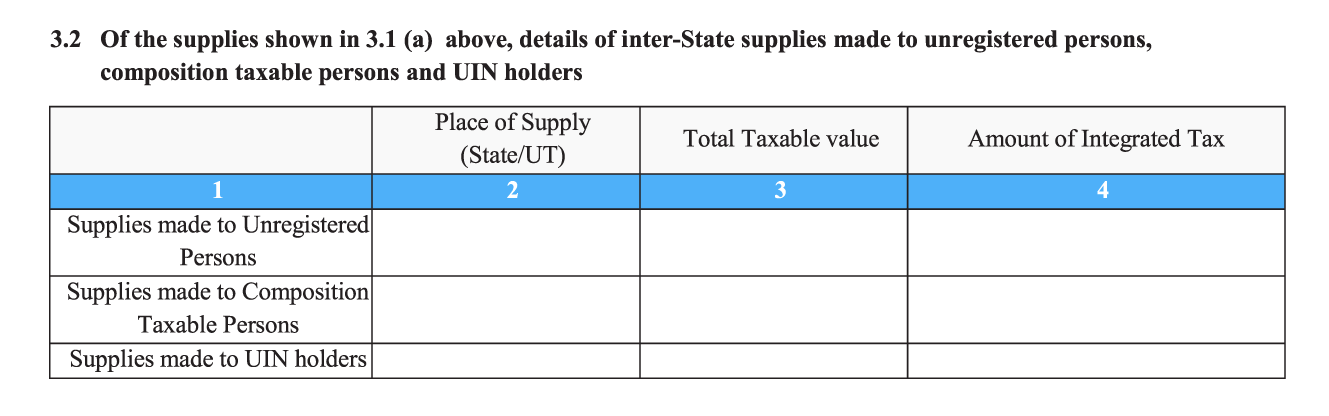

2. Details of inter-state sales made to unregistered buyers, buyers registered under the composition scheme, and UIN (Unique Identification Number) holders.

In this section, you will have to fill in details regarding the place of supply, total taxable value, and IGST for the following:

* Supplies made to unregistered people

* Supplies made to Composition Taxable people

* Supplies made to UIN holders

Unique Identification Number (UIN) holders include the following:

* Any specialized agency related to the United Nations Organization

* Consulates or embassies of foreign countries

* Multilateral Financial Institutions or Organizations included under the United Nations Organizations Privileges and Immunities Act of 1947

* Any person or group of people who have been designated by the Commissioner to receive a UIN

3. Eligible ITC (Input Tax Credit)

In this section, you will have to fill in details regarding the place of supply, total taxable value, and IGST for the following:

* Supplies made to unregistered people

* Supplies made to Composition Taxable people

* Supplies made to UIN holders

Unique Identification Number (UIN) holders include the following:

* Any specialized agency related to the United Nations Organization

* Consulates or embassies of foreign countries

* Multilateral Financial Institutions or Organizations included under the United Nations Organizations Privileges and Immunities Act of 1947

* Any person or group of people who have been designated by the Commissioner to receive a UIN

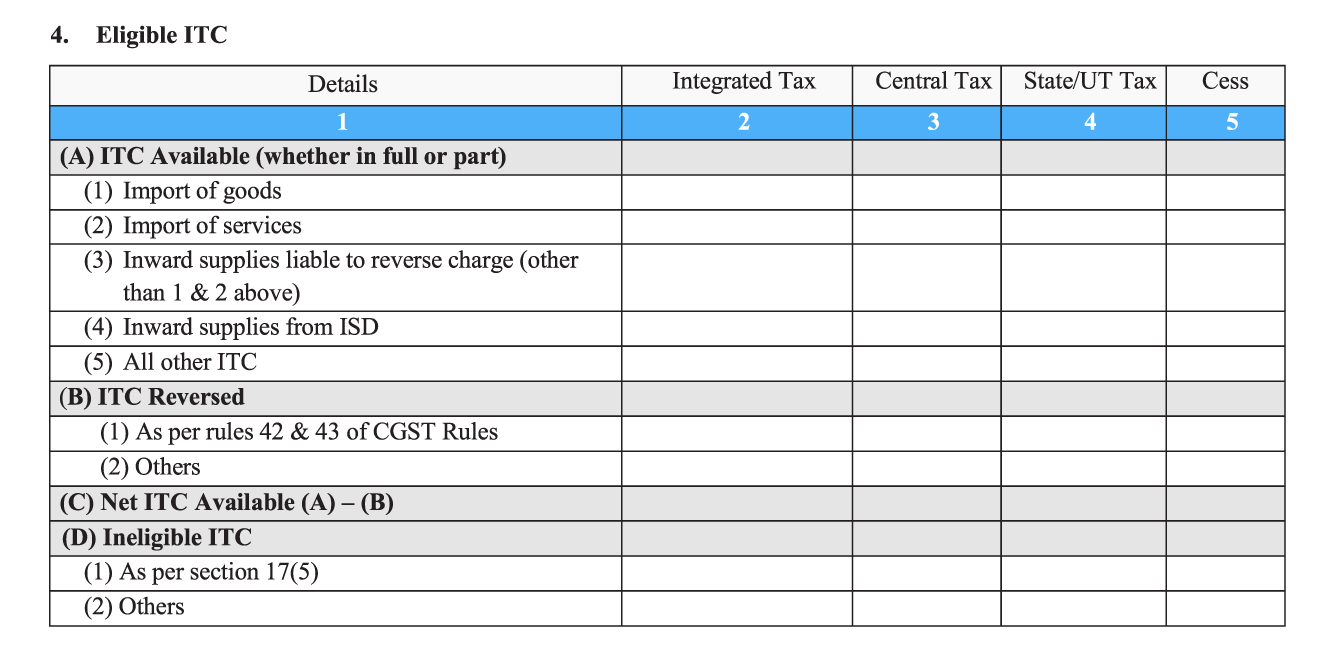

3. Eligible ITC (Input Tax Credit)

Your final tax payment and credits will be calculated based on your income tax credit (ITC). In this section, you will have to enter details about the following:

* ITC available (whether in full or part): Enter the tax amounts related to import of goods, import of services, inward supplies liable for reverse charge, inward supplies from Input Service Distributors, and all other ITC that is not included in (1) and (2), i.e- the above sections.

* ITC Reversed (per rules 43 and 44 of CGST rules): Under this you will have to furnish details regarding the utilization of goods/services for non-business purposes.

* Net ITC available: Calculate this by subtracting the reversed ITC from the available ITC.

Ineligible ITC (per section 17(5) and others): This includes blocked credits, which occur when certain services are involved. Transportation services (if they’re not for the purpose of supplying goods), food, health services, cab services, and beauty services can all result in blocked credits.

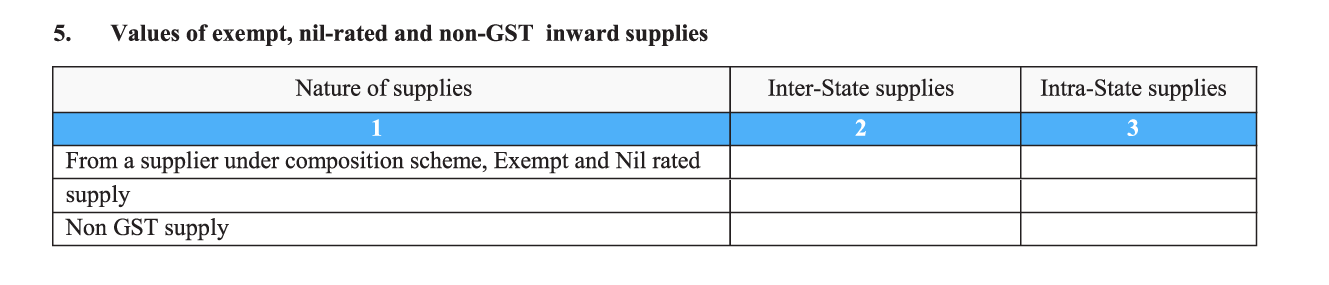

4. Values of exempt, nil-rated, and non-GST inward supplies

Your final tax payment and credits will be calculated based on your income tax credit (ITC). In this section, you will have to enter details about the following:

* ITC available (whether in full or part): Enter the tax amounts related to import of goods, import of services, inward supplies liable for reverse charge, inward supplies from Input Service Distributors, and all other ITC that is not included in (1) and (2), i.e- the above sections.

* ITC Reversed (per rules 43 and 44 of CGST rules): Under this you will have to furnish details regarding the utilization of goods/services for non-business purposes.

* Net ITC available: Calculate this by subtracting the reversed ITC from the available ITC.

Ineligible ITC (per section 17(5) and others): This includes blocked credits, which occur when certain services are involved. Transportation services (if they’re not for the purpose of supplying goods), food, health services, cab services, and beauty services can all result in blocked credits.

4. Values of exempt, nil-rated, and non-GST inward supplies

Under this sub-section, the taxpayer should enter taxation details for inter-state and intra-state supplies. This includes supplies purchased from a supplier under the Composition Scheme, and exempt, nil-rated and non-GST inward supplies.

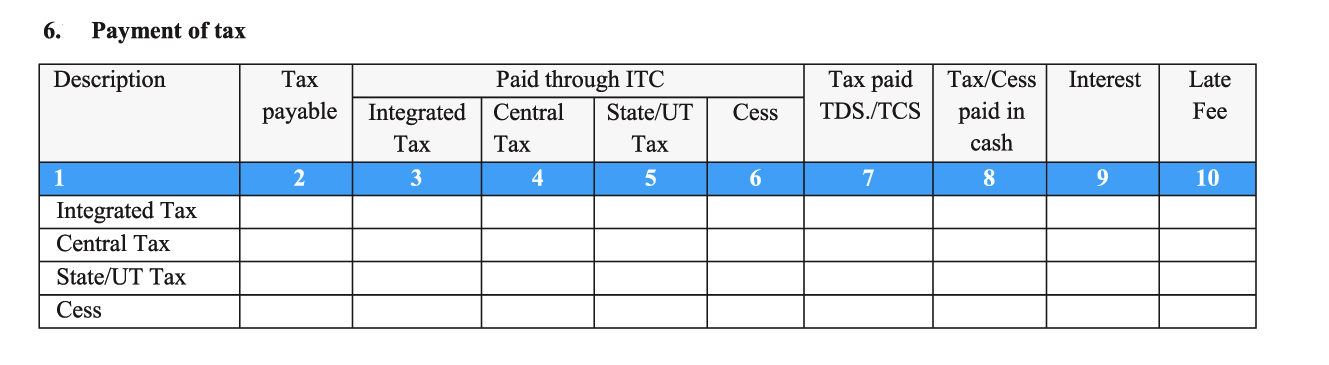

5. Payment of tax

Under this sub-section, the taxpayer should enter taxation details for inter-state and intra-state supplies. This includes supplies purchased from a supplier under the Composition Scheme, and exempt, nil-rated and non-GST inward supplies.

5. Payment of tax

This sub-section is where you will enter the overall tax amounts to be paid for CGST, SGST, IGST, and cess. Include the overall tax payable, tax paid through ITC, tax paid with respect to TDS/TCS, tax/cess that was paid in cash, interest, and late fee.

6. TDS/TCS credit

This sub-section is where you will enter the overall tax amounts to be paid for CGST, SGST, IGST, and cess. Include the overall tax payable, tax paid through ITC, tax paid with respect to TDS/TCS, tax/cess that was paid in cash, interest, and late fee.

6. TDS/TCS credit

Enter the corresponding values of IGST, CGST, and SGST with respect to the Tax Deducted at Source and Tax Collected at Source in this section.

After filling in all these details, the GSTR-3B form can be submitted after being signed by the authorized taxpayer.

Enter the corresponding values of IGST, CGST, and SGST with respect to the Tax Deducted at Source and Tax Collected at Source in this section.

After filling in all these details, the GSTR-3B form can be submitted after being signed by the authorized taxpayer.