What is a cash flow statement?

A cash flow statement is an important tool used to manage finances by tracking the cash flow for an organization. This statement is one of the three key reports (with the income statement and the balance sheet) that help in determining a company’s performance. It is usually helpful for making cash forecast to enable short term planning.

The cash flow statement shows the source of cash and helps you monitor incoming and outgoing money. Incoming cash for a business comes from operating activities, investing activities and financial activities. The statement also informs about cash outflows, expenses paid for business activities and investment at a given point in time. The information that you get from the cash flow statement is beneficial for the management to take informed decisions for regulating business operations.

Companies generally aim for a positive cash flow for their business operations without which the company may have to borrow money to keep the business going.

Importance of a cash flow statement

For a business to be successful, it should always have sufficient cash. This enables it to pay back bank loans, buy commodities, or invest to get profitable returns. A business is declared bankrupt if it doesn’t have enough cash to pay its debts. Here are some of the benefits of a cash flow statement:

-

Gives details about spending: A cash flow statement gives a clear understanding of the principal payments that the company makes to its creditors. It also shows transactions which are recorded in cash and not reflected in the other financial statements. These include purchases of items for inventory, extending credit to customers, and buying capital equipment.

-

Helps maintain optimum cash balance: A cash flow statement helps in maintaining the optimum level of cash on hand. It is important for the company to determine if too much of its cash is lying idle, or if there’s a shortage or excess of funds. If there is excess cash lying idle, then the business can use it to invest in shares or buy inventory. If there is a shortage of funds, the company can look for sources from where they can borrow funds to keep the business going.

-

Helps you focus on generating cash: Profit plays a key role in the growth of a company by generating cash. But there are several other ways to generate cash. For instance, when a company finds a way to pay less for equipment, it is actually generating cash. Every time it collects receivables from its customers quicker than usual, it is gaining cash.

-

Useful for short-term planning: A cash flow statement is an important tool for controlling cash flow. A successful business must always have sufficient liquid cash to fulfill short-term obligations like upcoming payments. A financial manager can analyze incoming and outgoing cash from past transactions to make crucial decisions. Some situations where decisions have to be made based on the cash flow include forseeing cash deficit to pay off debts or establishing a base to request for credit from banks.

Format of a cash flow statement

There are three sections in a cash flow statement: operating activities, investments, and financial activities.

Operating activities: Operating activities are those cash flow activities that either generate revenue or record the money spent on producing a product or service. Operational business activities include inventory transactions, interest payments, tax payments, wages to employees, and payments for rent. Any other form of cash flow, such as investments, debts, and dividends are not included in this section.

The operations section on the cash flow statement begins with recording net earnings, which are obtained from the net income field on the company’s income statement. This gives an estimate of the company’s profitability. After this, it lists non-cash items involving operational activities and convert them into cash items. A business’ cash flow statement should show adequate positive cash flow for its operational activities. If it doesn’t, the business may find it difficult to manage its daily business operations.

Investment activities: The second section on the cash flow statement records the gains and losses caused due to investment in assets like property, plant, or equipment (PPE) thus reflecting overall change in the cash position for a company. When analysts want to know the company’s investment on PPE, they check for changes on a cash flow statement.

Capital expenditure (CapEx) is another important line item under investment activities. CapEx is the money which a business invests on fixed assets like buildings, vehicles or land. An increase in CapEx means the company is investing on future operations. However, it also shows that there is a decrease in company cash flow.

Sometimes a company may experience negative cash flow due to heavy investment expenditure, but this is not always an indicator of poor performance, because it may be leading to high capital growth.

Financial activities: The third section on the cash flow statement records the cash flow between the company and its owners and creditors. Financial activities include transactions involving debt, equity, and dividends. In these transactions, incoming cash is recorded when capital is raised (such as from investors or banks), and outgoing cash is recorded when dividends are paid.

Cash flow statement example

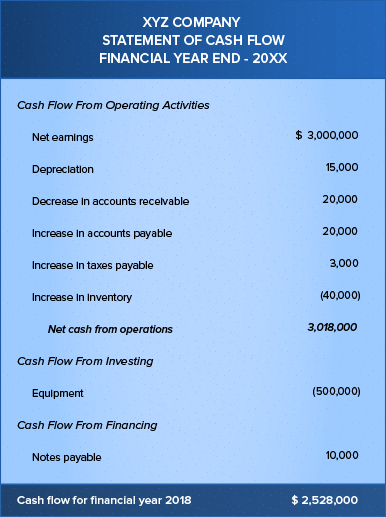

Following is an example of what a cash flow statement looks like. This is the cash flow statement for XYZ company at the end of Financial Year (FY) 2018.

From the above example, we can see that the computed cash flow for FY 2018 was $ 2,528,000. Let’s look at what each section is showing.

Operating activities: In this section, we can see incoming cash values recorded as positive while outgoing cash values are negative and are usually represented in brackets. When you subtract the outgoing value from the incoming value, you arrive at the net cash flow for operating activities. In this example, we can see that the net value for operating activities is positive, which is a good sign for investors.

Investing activities: Since the core operating activities are generating income, the business can now invest in equipment. Because the company is investing $500,000 in equipment, its cash flow in this section is negative. This negative value isn’t a bad thing—you can say that the company’s capacity to invest in PPE reflects its growth.

Financial activities: After investing in equipment, the company still has $10,000 to pay off its debts—in this case, notes payable. Besides this the company will still have plentiful to cover its loans in future.

Net cash flow: When you add all three net values from the three sections on the cash flow statement, you arrive at the net cash flow value, which in this case is $ 2,528,000. This shows that the company has enough cash to continue operating.

What is negative cash flow?

Negative cash flow is a situation where a company has more outgoing cash than incoming cash. The money that the company is earning from sales may not be enough to cover its expenses, and it may have to borrow from external sources to cover the differences.

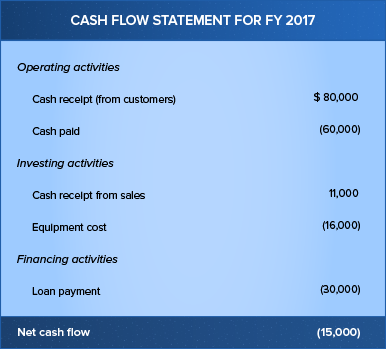

Following is a small example showing negative cash flow. Here you can see that the business paid more in expenses than the amount of income it brought in.

A negative cash flow doesn’t always imply that the company’s financial performance was bad. Sometimes the company’s incoming profit might be good, yet there is little money in the bank to pay off debts. Negative cash flow is common for small businesses, but it is unhealthy if it goes on for a long period.

Conclusion

A cash flow statement is a valuable document for a company, as it shows whether the business has enough liquid cash to pay its dues and invest in assets. You cannot interpret a company’s performance just by looking at the cash flow statement. You may need to analyse long term trends after referring to balance sheet and income statement in order to get a somewhat clear picture of how the company is faring.