Every business that does bookkeeping needs to record its transactions somewhere. When you have multiple customers and vendors, it can be a hectic task to consolidate all your sales and purchases in just a notebook. You need organization, so when tax or audit season rolls around, you are not left scrambling at the last minute. Transaction records are important because they are proof of how your money is being exchanged, how regularly, and with whom. But where do you record the movement of money to and from your business? Also, how do you record uncommon transactions like depreciation, bad debt, and the sale of assets? This is where journals and ledgers come into play. Read on to find out more about them and how you can use them for your business.

The journal. What is it?

The journal is also known as the book of original entry. It is where a business transaction is recorded when it first happens. A journal can be physical or electronic, and sales, purchases, or any movement of money to or from your business is recorded in chronological order. A journal contains the following information:

- The date of the transaction

- The account or accounts that are debited, and the amount involved

- The account or accounts that are credited, and the amount involved

- A short description and reference of the transaction

The golden rules of accounting

Every journal entry that is made must follow the golden rules of accounting. These rules apply to three specific accounts. Let’s define these accounts and take a look at their associated rules:

Real account – an account that pertains to assets and liabilities.

- Golden Rule: Debit what comes into the business, and credit what goes out of the business.

Personal account – includes all accounts related to individuals, firms, and associations.

- Golden Rule: Debit the receiver, and credit the giver.

Nominal account – related to all income, expenses, losses and profits.

- Golden Rule: Debit the expense or loss, and credit the income or profit.

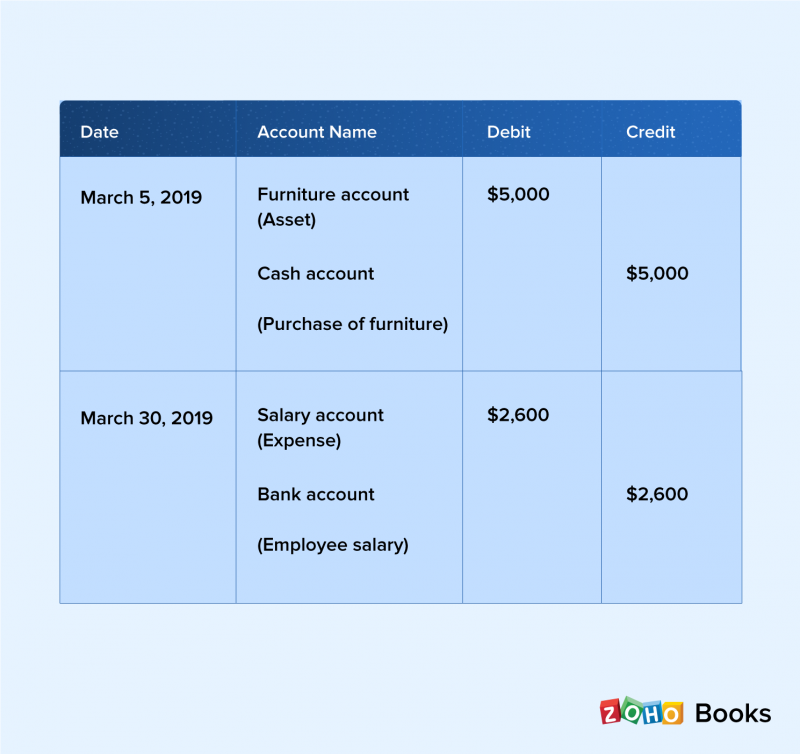

Journal entries – format & example

Using the accounts and rules above, let’s see how entries are made in the journal.

On March 5th, you buy furniture for your office worth $5,000 in cash. The furniture is considered an asset, so this is affecting the real account. The golden rule states that assets are debited, so you add $5,000 to the debit column of the journal. An equal credit must be recorded to the cash account, so you add $5,000 to the credit side of the journal. Finally, you note down the description of the transaction as a purchase of furniture worth $5,000.

On March 30th, the nominal account was debited for salary expenses, and the business’ bank account was credited to reflect that. You can see that the transactions entered in the journal follow the golden rules of accounting.

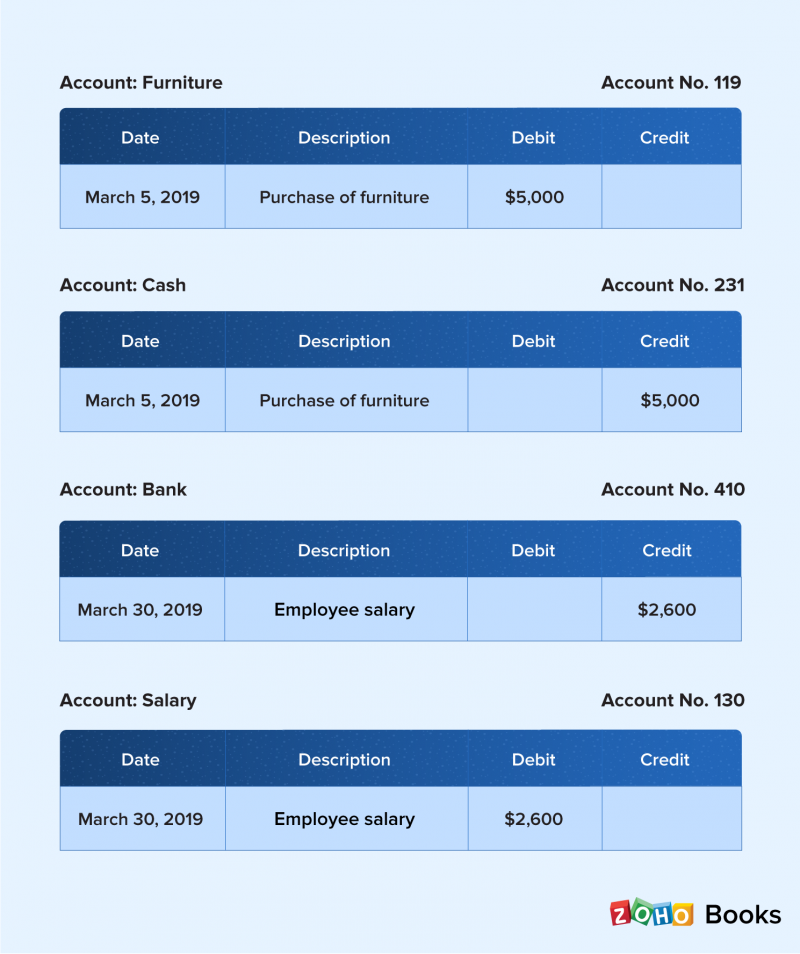

The ledger. What is it?

The ledger is also known as the book of second entry or the principal book of accounts. The ledger contains the chart of accounts, which is the list of all names and account numbers in the ledger. The ledger is given special importance by auditors and must be “balanced,” where the total debits always equals the total credits. If the debits outweigh the credits, it is called a debit balance. If the credits are more than the debits, there is a credit balance.

Ledger entries – format & example

Transactions in the journal are grouped by accounts in the order of assets, liabilities, equity, income, and expenses. They are then transferred to the ledger. Ledger entries appear in the order of accounts compared to the journal’s chronological order.

What comes after the journal and ledger?

After you have categorized transactions into corresponding accounts and recorded them in your ledger, you must check if your books are balanced. The trial balance helps you with that. It shows the ending balances of all your accounts as they appear on the balance sheet. The trial balance contains a description, account number, account name, debit balance, and credit balance. Once information from the ledger is consolidated into the trial balance, it is easy for your accountant to spot imbalances between debits and credits. It is concise, orderly, and helps remove discrepancy, proving to be a handy tool in keeping your books balanced.

Your books are balanced. Now what?

Once your books are balanced, it is time to generate financial reports to better understand how your business is performing. Every business must be aware of its growth and where it stands at any given point in time. Financial reports provide this insight. The cash flow statement depicts your cash flow trends by showing you how money moves in and out of your business. The balance sheet tells you how much your business owns, how much it owes, and its shareholder’s equity. The income statement, or profit and loss statement, focuses on the revenue gained and expenses incurred by a business over time. These are the three reports that businesses must pay most attention to.

The importance of journals and ledgers

Why is there so much emphasis on using journals and ledgers? The answer is simple. You can accomplish your bookkeeping goals easier when you have complete records of all your transactions. Financial statements like the cash flow statement, balance sheet, and income statement provide vital information about your business trends, and they can only be generated by using information from journals and ledgers. Recording and tracking uncommon transactions like depreciation, bad debt, and the sale of assets are made easier with journals. Journals and ledgers also help you to capture both the debit and the credit sides of transactions. This is often overlooked when companies do not use books.

The bottom line

Recording business transactions forms the core of your bookkeeping. It does not make sense to record them only when taxes and audits are around the corner. Ensuring accurate accounts of your business requires diligent upkeep of journals and ledgers. They are important and useful tools that keep you on track and allow you to set performance goals. Most importantly, they help you as a business owner to understand your company’s financial operations so you can assess growth and maintain a healthy and thriving organization.